Often times when we look to the government for answers, we are only given unofficial information or opinions. The IRS will tell us the law and point us to their website, though their own manual tells their employees that their website is not the law and only used as an interpretive guide to make things simpler for us to understand. However, this is part of a grand deception. We should never trust an agent of the government, and always go directly to the source. Here are some of the most important cases and laws that destroy the narrative that we all have to pay taxes, just because the IRS says so.

The power to tax is the power to destroy

That the power to tax involves the power to destroy; that the power to destroy may defeat and render useless the power to create.

McCulloch v. Maryland, 17 U.S. 316 (1819)

Trading property and labor is a right

Included in the right of personal liberty and the right of private property, partaking of the nature of each, is the right to make contracts for the acquisition of property, chief among which is that of personal employment by which labor and other services are exchanged for money or other forms of property.

Coppage v. Kansas, 236 US 1 (1915)

Rights can not be taxed

A State may not impose a charge for the enjoyment of a right granted by the Federal Constitution.

Murdock v Pennsylvania, 319 US 105 (1943)

Working is a right

The right to follow any of the common occupations of life is an inalienable right, it was formulated as such under the phrase “pursuit of happiness” in the declaration of independence, which commenced with the fundamental proposition that “all men are created equal; that they are endowed by their Creator with certain inalienable rights; that among these are life, liberty, and the pursuit of happiness.”

Butchers’ Union Co. v. Crescent City Co., 111 U.S. 746 (1884)

Labor is Property

the property which every man has in his own labor, as it is the original foundation of all other property, so it is the most sacred and inviolable. The patrimony of the poor man lies in the strength and dexterity of his own hands, and to hinder his employing this strength and dexterity in what manner he thinks proper, without injury to his neighbor, is a plain violation of this most sacred property. It is a manifest encroachment upon the just liberty both of the workman and of those who might be disposed to employ him. As it hinders the one from working at what he thinks proper, so it hinders the others from employing whom they think proper.

Butchers’ Union Co. v. Crescent City Co., 111 U.S. 746 (1884) – Quoting Adam Smith’s The Wealth of Nations

Privileges (not rights) can be restricted through taxation

The power to tax the exercise of a privilege is the power to control or suppress its enjoyment.

A. Magnano Co. v. Hamilton, 292 U.S. 40 (1934)

Since the right to receive income or earnings is a right belonging to every person, this right cannot be taxed as privilege.

Jack Cole Co. v. MacFarland, 206 Tenn. 694, 337 S.W.2d 453 (Tenn. 1960)

Rights can not be treated as privileges

the Legislature has no power to declare as a privilege and tax for revenue purposes occupations that are of common right, but it does have the power to declare as privileges and tax as such for State revenue purposes those pursuits and occupations that are not matters of common right, and to declare and tax as a privilege for State revenue any other subjects or sources of taxation that are not pursuits or occupations of common right.

Sims v. Ahrens, 167 Ark. 557 (1925)

Income tax only applies to privileges

by the previous ruling, it was settled that the provisions of the Sixteenth Amendment conferred no new power of taxation, but simply prohibited the previous complete and plenary power of income taxation possessed by Congress from the beginning from being taken out of the category of indirect taxation to which it inherently belonged, and being placed in the category of direct taxation subject to apportionment by a consideration of the sources from which the income was derived — that is, by testing the tax not by what it was, a tax on income, but by a mistaken theory deduced from the origin or source of the income taxed.

Stanton v. Baltic Mining Co., 240 U.S. 103 (1916)

There is no room to assume the meaning of the law

But it matters little what it does mean; the statute and the statute alone determines what is income to be taxed.

…

It taxes only income “derived” from many different specified sources; one does not “derive income” by rendering services and charging for them.

Edwards v. Keith, 231 F. 110 (1916)

In the interpretation of statutes levying taxes, it is the established rule not to extend their provisions by implication beyond the clear import of the language used, or to enlarge their operations so as to embrace matters not specifically pointed out. In case of doubt, they are construed most strongly against the government and in favor of the citizen.

Gould v. Gould, 245 U.S. 151 (1917)

Income is not everything that comes in

We must reject in this case, as we have rejected in cases arising under the Corporation Excise Tax Act of 1909 (Doyle v. Mitchell Brothers Co., ante, 247 U. S. 179, and Hays v. Gauley Mountain Coal Co., ante, 247 U. S. 189), the broad contention submitted in behalf of the government that all receipts — everything that comes in — are income within the proper definition of the term “gross income,” and that the entire proceeds of a conversion of capital assets, in whatever form and under whatever circumstances accomplished, should be treated as gross income. Certainly the term “income” has no broader meaning in the 1913 act than in that of 1909 (see Stratton’s Independence v. Howbert, 231 U. S. 399, 231 U. S. 416-417), and, for the present purpose, we assume there is no difference in its meaning as used in the two acts.

Southern Pacific Co. v. Lowe, 247 U.S. 330 (1918)

Social Security does not have its own fund

26 USC 3501 (a)General rule

Title 26

The taxes imposed by this subtitle shall be collected by the Secretary and shall be paid into the Treasury of the United States as internal-revenue collections.

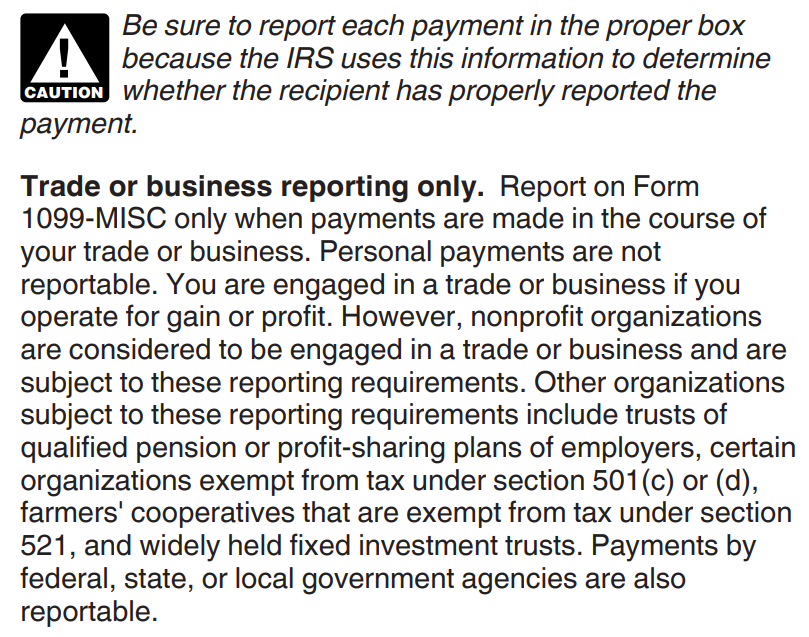

Are you engaged in a trade or business?

Instructions for form 1099-MISC / NEC

Self Employment means “trade or business”

26 USC 1402(a) Net earnings from self-employment

Title 26

The term “net earnings from self-employment” means the gross income derived by an individual from any trade or business carried on by such individual…

“Trade or business” means working for the government.

26 USC 7701(a)(26) Trade or business The term “trade or business” includes the performance of the functions of a public office.

Title 26

Do not fear criminal charges

A good-faith misunderstanding of the law or a good-faith belief that one is not violating the law negates willfulness, whether or not the claimed belief or misunderstanding is objectively reasonable.

Cheek v. United States, 498 U.S. 192 (1991)

Laws may remain only if they can be interpreted constitutionally.

No court ought, unless the terms of an act of Congress render it unavoidable, to give a construction to the act which should, however unintentional, involve a violation of the Constitution.

Parsons v. Bedford, Breedlove & Robeson, 28 U.S. 433 (1830)

Although research has shown and practice has established the futility of the charge that it was a usurpation when this Court undertook to declare an Act of Congress unconstitutional, I suppose that we all agree that to do so is the gravest and most delicate duty that this Court is called on to perform. Upon this among other considerations, the rule is settled that, as between two possible interpretations of a statute, by one of which it would be unconstitutional and by the other valid, our plain duty is to adopt that which will save the Act.

Blodgett v. Holden, 275 U.S. 142 (1927)